What is the Event Logistics Market Overview – definition, scope, and significance?

The Event Logistics Market encompasses all services and solutions required to plan, transport, store, and manage assets for live events, ranging from concerts and sports tournaments to corporate exhibitions and cultural festivals. It includes inventory management, delivery coordination, freight forwarding, and specialized pallets and packaging services that ensure equipment, stages, lighting, and merchandise reach venues safely and on schedule. The scope of the market extends across the entire event life‑cycle, covering pre‑event procurement, on‑site logistics, and post‑event teardown and return. Its significance lies in enabling seamless attendee experiences, protecting valuable assets, and reducing operational risks, which in turn drives revenue growth for event organizers, venues, and logistics providers worldwide.

What are the primary drivers, restraints, challenges, and opportunities shaping the Event Logistics Market?

Key drivers include the rising frequency of large‑scale live events, growing consumer demand for immersive experiences, and increased outsourcing of logistics to specialist firms that can guarantee reliability and compliance. Technological advancements such as real‑time tracking and AI‑based routing further boost efficiency. Restraints stem from high capital requirements for specialized equipment and the seasonal nature of many events, which can lead to underutilized assets during off‑peak periods. Challenges involve navigating complex regulatory environments across borders, handling fragile or high‑value equipment, and mitigating risks associated with weather or security incidents. Opportunities arise from the expansion of hybrid events that combine physical and virtual elements, the adoption of sustainable packaging and carbon‑neutral transportation solutions, and the emergence of smart warehousing technologies that can provide competitive differentiation.

What are the current growth trends in the Event Logistics Market?

Current trends include a shift toward integrated logistics platforms that offer end‑to‑end visibility for event planners, allowing them to coordinate inventory, delivery, and on‑site handling from a single dashboard. There is also a notable increase in the use of modular and reusable packaging, driven by sustainability goals and cost‑efficiency pressures. Another emerging trend is the deployment of autonomous vehicles and drones for last‑mile delivery of lightweight assets, which can reduce lead times and labor costs. Finally, data analytics is being leveraged to predict demand spikes, optimize routing, and improve resource allocation for recurring events such as annual festivals and sports leagues.

How did COVID‑19 impact the Event Logistics Market and what is the recovery trajectory?

The pandemic caused a severe contraction in live‑event activity, leading to a steep decline in logistics demand as concerts, sports matches, and trade shows were postponed or canceled. Supply chains faced disruptions, and many logistics providers pivoted to alternative segments such as e‑commerce fulfillment. Recovery began in late 2021 as vaccination rates rose and restrictions eased, with a gradual resurgence of in‑person events. The market is now experiencing a rebound, supported by pent‑up consumer demand and the introduction of hybrid event formats that blend physical attendance with virtual streaming, creating new logistics requirements for both on‑site equipment and remote delivery of digital assets.

Who are the major competitors and what is the level of consolidation in the Event Logistics Market?

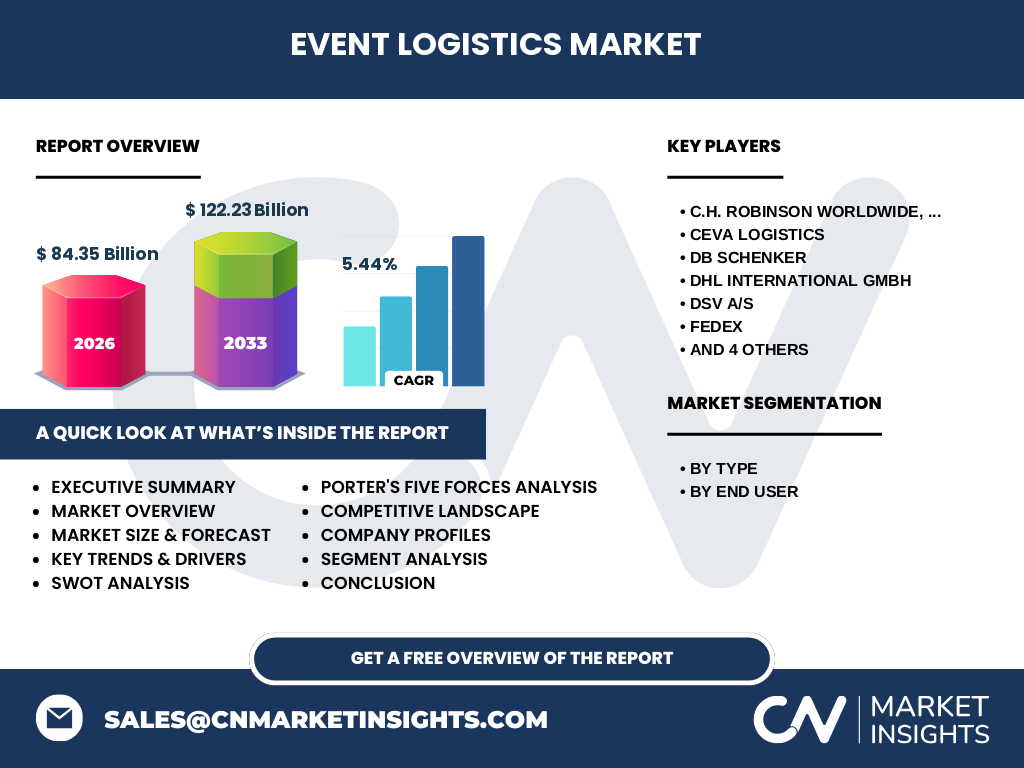

The competitive landscape is dominated by global logistics giants with dedicated event‑service divisions. Key players include C.H. Robinson Worldwide, Inc., CEVA Logistics, DB Schenker, DHL International GmbH, DSV A/S, FedEx, Kuehne+Nagel, Rhenus Group, United Parcel Service of America, Inc., and XPO Logistics, Inc. These firms leverage extensive networks, technology platforms, and specialized expertise to capture large contract values. The market has seen moderate consolidation, with several mergers and acquisitions aimed at expanding geographic reach and adding event‑specific capabilities, thereby intensifying competition for high‑profile contracts.

What are the key findings highlighted in the Executive Summary?

The Executive Summary reveals that the Event Logistics Market is valued at $84.35 billion in 2026 and is projected to reach $122.23 billion by 2033, reflecting a compound annual growth rate (CAGR) of 5.44 %. Growth is driven by increasing live‑event volumes, the rise of hybrid formats, and technology‑enabled efficiency gains. Sustainability and the need for resilient, real‑time logistics solutions present significant opportunities. Competitive pressure is intensifying as major logistics providers expand dedicated event services, while smaller niche operators focus on specialized segments such as cultural festivals or boutique corporate events.

What is the forecast for the Event Logistics Market from 2025 to 2032?

Based on the provided data, the market is expected to maintain a steady upward trajectory, expanding from its 2026 base of $84.35 billion to $122.23 billion by the end of the forecast horizon in 2033. This growth corresponds to a CAGR of 5.44 %, indicating consistent demand across all event categories. The forecast assumes continued recovery from pandemic disruptions, ongoing investment in logistics technology, and expanding event portfolios in emerging economies.

How is the Event Logistics Market sized and shared by type and end‑user segmentation?

Segmentation by type includes Inventory Management, Delivery Management, Freight Forwarding, and Pallets and Packaging Services. By end‑user, the market is divided into Media and Entertainment, Sports Events, Corporate Events and Trade Fairs, and Cultural Events. While exact numeric shares are not disclosed, each segment plays a critical role: Inventory Management ensures accurate tracking of assets; Delivery Management coordinates timely transport; Freight Forwarding handles cross‑border shipments; and Pallets and Packaging Services provide protection and compliance. End‑users such as Media and Entertainment and Sports Events typically generate the highest logistics volumes due to large stage setups and equipment needs, whereas Cultural Events and Corporate Trade Fairs rely heavily on specialized packaging and inventory control.

What is the global geographic distribution of the Event Logistics Market?

The market exhibits a worldwide footprint, with major activity concentrated in regions that host large‑scale live events, including North America, Europe, and Asia‑Pacific. These regions benefit from established venue infrastructures, advanced logistics networks, and high consumer spending on entertainment and corporate gatherings. Emerging markets in Latin America and the Middle East are showing growth potential as they increase investments in event venues and attract international touring productions.

What does the regional analysis of the Event Logistics Market reveal?

North America leads in terms of total spend, driven by a mature entertainment industry, frequent sports championships, and a dense concentration of trade fairs. Europe follows closely, with strong cultural festivals and a robust corporate events calendar. Asia‑Pacific displays the fastest growth rate, propelled by expanding middle‑class populations, rising tourism, and government initiatives to host global sporting events and expos. Latin America and the Middle East, while smaller in absolute terms, are experiencing incremental growth thanks to new venue constructions and increased international event hosting.

What are the profiles and strategies of leading companies in the Event Logistics Market?

Leading firms such as DHL International GmbH and FedEx leverage global carrier networks and advanced tracking platforms to provide end‑to‑end visibility for event assets. Kuehne+Nagel focuses on integrated supply‑chain solutions, combining freight forwarding with inventory management software tailored for large productions. CEVA Logistics emphasizes value‑added services like on‑site handling and temporary storage. Companies like XPO Logistics and United Parcel Service are investing in last‑mile innovations, including autonomous delivery and climate‑friendly transport options, to differentiate their event‑logistics offerings.

How does Porter’s Five Forces analysis apply to the Event Logistics Market?

Threat of new entrants is moderate; high capital requirements and the need for specialized expertise create barriers, yet niche players can enter by focusing on specific event types. Bargaining power of suppliers is low to moderate because logistics firms often own or lease key assets such as trucks and containers. Bargaining power of buyers is relatively high, as event organizers demand cost‑effective, on‑time delivery and can switch providers. Threat of substitutes remains low, given the specialized nature of event logistics compared with generic freight services. Industry rivalry is intense, with major global carriers competing for high‑visibility contracts and seeking differentiation through technology and sustainability initiatives.

What are the SWOT insights for the Event Logistics Market?

Strengths: Established global networks, advanced technology platforms, and experience handling high‑value, time‑critical assets. Weaknesses: Seasonal demand fluctuations and reliance on large‑scale events. Opportunities: Growth of hybrid events, demand for sustainable packaging, and adoption of AI‑driven optimization tools. Threats: Economic downturns affecting discretionary spending on events, regulatory changes impacting cross‑border freight, and potential disruptions from health crises.

What does the value chain of the Event Logistics Market look like?

The value chain begins with event planning and procurement, where requirements for stages, lighting, and merchandise are defined. This is followed by inventory management, featuring tagging, warehousing, and preparation of assets. The next stage is freight forwarding and transportation, encompassing domestic and international movement. Upon arrival, pallets and packaging services protect goods during handling, and delivery management coordinates last‑mile distribution to venues. On‑site logistics manage setup, real‑time monitoring, and contingency handling. Finally, post‑event teardown, return logistics, and reverse‑supply processes complete the cycle.

What key investment insights can be drawn from the Event Logistics Market?

Investors should focus on companies that are integrating digital platforms for real‑time visibility, as this capability is becoming a prerequisite for winning large contracts. Sustainable logistics solutions, such as reusable packaging and low‑emission transport, are gaining importance and may attract ESG‑focused capital. Acquisitions of niche players with specialized expertise in cultural or sports events can provide immediate market entry and diversified revenue streams. Lastly, expanding service portfolios to include hybrid‑event support—covering both physical assets and digital content logistics—offers significant upside.

What conclusions can be drawn about the Event Logistics Market?

The Event Logistics Market is on a robust growth path, driven by a resurgence of live events, technological innovation, and heightened sustainability expectations. With a projected market size of $122.23 billion by 2033 and a CAGR of 5.44 %, the sector presents attractive opportunities for both established logistics providers and new entrants that can deliver specialized, technology‑enabled, and environmentally responsible services.

How was the research methodology designed for this market report?

The study employed a mixed‑method approach, combining secondary data collection from industry publications, company annual reports, and reputable market databases with primary insights gathered through interviews with event organizers, logistics managers, and technology vendors. Quantitative analysis involved trend extrapolation using the provided base year (2026) value and the forecast figure for 2033, resulting in the calculated CAGR. Qualitative assessments were applied to evaluate competitive dynamics, strategic initiatives, and emerging technologies.

What is the scope of the research and its limitations?

The research scope covers global event‑logistics activities across all major event categories, segmented by service type and end‑user. It focuses on the period up to 2033, using the supplied market size and forecast figures. Limitations include reliance on publicly available information, which may not capture confidential contract values, and the exclusion of granular regional revenue breakdowns beyond the high‑level geographic overview.

Which key companies are highlighted and what recent developments have they announced?

Prominent firms include C.H. Robinson Worldwide, Inc., CEVA Logistics, DB Schenker, DHL International GmbH, DSV A/S, FedEx, Kuehne+Nagel, Rhenus Group, United Parcel Service of America, Inc., and XPO Logistics, Inc. Recent developments feature DHL’s launch of a carbon‑neutral event‑logistics service, FedEx’s pilot of autonomous delivery robots for on‑site equipment handling, and Kuehne+Nagel’s partnership with an AI‑analytics provider to enhance real‑time inventory tracking for large‑scale festivals. XPO Logistics announced an expansion of its temperature‑controlled fleet to support perishable goods at culinary events, while CEVA Logistics secured a multi‑year contract to manage freight for a major international sports league.